by Robert Montgomery 14th July 2020

“Why is the world financial system in crisis? First in 2008 and now in 2020 we have seen the world plunge into the worst financial crisis since the Great Depression with incalculable economic and political consequences. Marx’s work has a theory of economic crisis that explains why capitalism is inevitably convulsed by the boom and bust cycle and all the chaos that entails. This article aims to provide a brief introduction to Marx’s crisis theory. It begins with a brief overview, before examining Marx’s view that crises arise from the drive for an ever higher productivity of labor, which leads to a crisis of profitability. The tendency to crisis is rooted in the exploitation of living labor which is the lifeblood of capitalism. This article attempts to summarize Marx’s theory of the economic cycle and why periodic crises happen.”

General Overview

For Marx the process of capital accumulation leads eventually to an overaccumulation, or overproduction of capital. More capital accumulates in the hands of the ruling class than can be reinvested to yield a sufficient mass and rate of profit. This decreased profitability gives rise to a financial crisis. The circuit of capital is interrupted at many points. Creditors call in loans, hike interest rates, and choke off credit. The financial crisis leads to the devaluation of capital in many forms: writing off existing loans, lowering share values, allowing currencies to fall in value, business closings, unemployment, falling wages, and an overproduction of commodities.

We will start with a review of Marx’s theory of value, survey some objections to Marx’s claim, and then apply the theory in a more concrete way to describe how crises actually happen.

The Theory of Value

“Every child knows a nation which ceased to work, I will not say for a year, but even for a few weeks, would perish. Every child knows, too, that the masses of products corresponding to the different needs require different and quantitatively determined masses of the total labor of society…. Science consists precisely in demonstrating how the law of value asserts itself.” Marx to Kugelmann 1868

To understand crisis we have to start with the labor theory of value. In Capital v.1, Marx argues that the commodity has a dual nature— it is both a use value and an exchange value. If a commodity had no use for us, there wouldn’t be a demand for it. Because use values are qualitatively distinct, they lack a measurable relation to each other that would allow them to exchange in any proportion. Nevertheless, every useful commodity must be exchanged for other commodities. Exchange implies a common component that is quantitatively measurable, or commensurable. This common component is labor time. The value of commodities is determined by the average labor time expended in their production. Marx called this the labor time socially necessary to produce something at a given time and working at the level of skill and technology in use. Commodities exchange on average at this value.

This holds true for labor power, the only commodity owned and sold by the working class. Different from all other commodities, labor-power is the only one that adds new value to the material it works with. When labor-power is applied to other commodities— machinery and raw materials for example— it adds labor-time to them, which is the measure of value. If labor power is the only commodity that the mass of the working class owns and sells, then what is its value? Like other commodities, the value of labor power is determined by the labor time necessary for its production. For labor power this is the value of the basket of consumption goods needed to keep the worker alive and able to return to work the next day, and to live at the level of culture achieved by the working class in a given country. An expectation of what is needed to keep a worker going differs from one society to another. The expectations and requirements to reproduce the labor of a worker in Detroit and a worker in Mumbai are different. The value of labor power is therefore lower in some countries than others. The value of labor power is governed by the cost of reproducing the laborer, not by the value of the product itself.

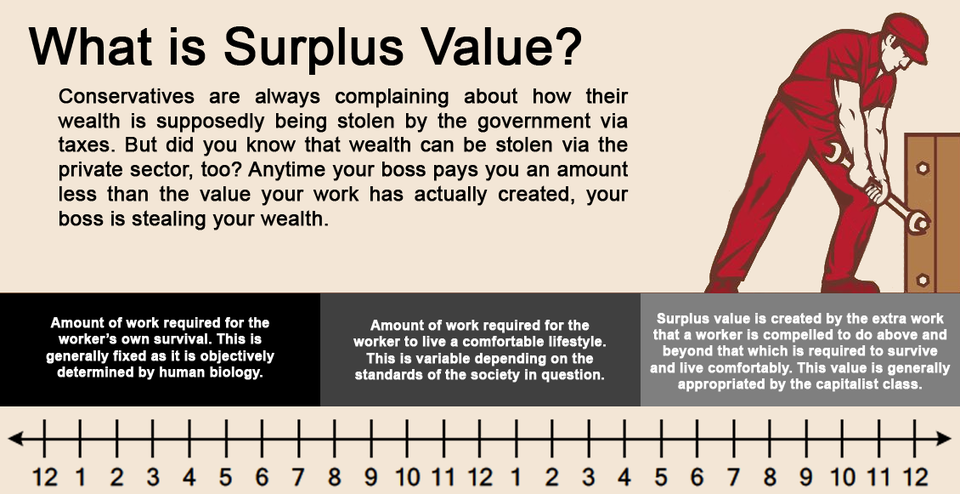

We can think of the working day as divided into two parts. The first part is necessary labor time, the period during which the worker produces value equivalent to the cost of reproducing his or her labor power. This labor time is less than the length of the working day. The other part of the working day is surplus labor time. This is the unpaid part of the working day in which surplus value is produced. Surplus value is the source of profit.

Necessary labor time is only one part of the working day. If I work until I produce enough value to equal my wages, I could clock out at noon. Capitalists purchase labor to make a profit. If I only earn the value of my wages, the employer has no reason to hire me. So the value of labor power is less than the value the worker adds to the mass of products produced. The remainder is surplus value the capitalist accumulates as profit. Labor power generates surplus value because a portion of the worker’s labor time is unpaid. In the course of accumulating capital, competition forces capitalists to increase the productivity of labor, enabling more to be produced in less time. The most obvious way of doing this is by introducing new and more advanced machinery. This reduces the time needed for the worker to produce a commodity. The average labor time needed to make a product lessens, and the value of the commodity falls. The first capitalist to introduce a newer technique makes a windfall profit as the more cheaply produced commodities sell on the market either at the previous price, or below it. As more products are produced in a given time, less time is needed for the worker to generate enough value to cover his or her cost of living. Therefore, the part of the working day that makes up the necessary labor time is reduced. While the necessary labor time falls, the surplus labor time expended during a working day rises proportionately, and the capitalist’s profit increases.

Capitalism therefore has an intrinsic drive to increase labor productivity by raising the level of technology used in production. In Marx’s terms, there is a drive to raise the proportion of constant capital (machinery and raw materials) to variable capital (living labor). This boosts the share of profits of the more productive capitalist. To stay in business, competing capitalists in the same branch of production must introduce the same innovation, removing the short-term advantage gained in the market by the first capitalist. But at the same time, something very important has happened. The proportion of capital invested in living labor has fallen relative to the proportion spent on machinery and raw materials. So the constant capital has risen in proportion to the variable capital. Marx calls this an increase in the organic composition of capital, or simply c/v.

This tendency has important consequences for the system of profit generation. Marx established that the source of profit is surplus value, the unpaid labor-time of the worker. Since only the worker produces surplus value, it is only the investment in variable capital that generates profit. The constant capital— machinery, buildings, raw materials and semi-finished goods used — are themselves products of wage labor. A capitalist earlier in the production chain has already pocketed the profit from the surplus labor expended in their production. The constant capital does not add extra value to products that did not exist before; it just transfers stored value to the new product as its value slowly depreciates with each cycle of production. It is only variable capital, representing human labor power that creates new value.

Imagine a Foxconn factory producing smartphones. By increasing the productivity of labor, new technology allows the same labor force to make more smartphones per hour. As the socially necessary labor time embodied in each item falls, the value of each smartphone decreases relative to the value of the competitor’s phones, and Foxconn makes a more profit than its competitors. The new technology appears to have increased value generation, but it has simply transferred the value created by the original labor used to make the new machines. As time goes by, the new machinery keeps transferring its value to new products, and slowly depreciates in value itself. Because it merely transfers the value stored in it to new commodities, Marx called this constant capital because its value remains unchanged. The process recurs as a continual drive to increase labor productivity by introducing new technology, or expressed in value terms, by increasing the constant capital employed in production. However, this process does not simply occur in a single smartphone factory but across all capitalist production, including in the factory that made the machine, which increased Foxconn’s productivity in the first place. This expresses a general tendency in capitalism for constant capital to increase in proportion to the variable capital, although the variable capital is the sole factor creating new value.

Overaccumulation of Capital and the Falling Rate of Profit

Law of the tendency of the rate of profit to fall

“In every respect the most important law of modern political economy and the most essential for understanding the most difficult relations. It is the most important law from the historical standpoint. It is a law, which despite its simplicity, has never before been grasped and even less consciously articulated.” Marx, Grundrisse

At the most abstract level capital is self-expanding value. In the process of self-expansion capital goes through a series of different forms. The general formula is M-C-M:

● Money buys commodities in the form of means of production and labor power

● Means of production and labor power combine to produce commodities for exchange in the market, which when sold yield profit

● Profit appears in the form of an expanded sum of money that is then re-invested to return even more profits.

In the process value has expanded. To accumulate the additional value as profit, capital appropriates unpaid labor (surplus value or “s”), the only source of profit. It’s essential to keep in mind that this process occurs through the exchange of commodities in the competitive market. Competition drives capitalists to constantly invest in more productive technology in order to appropriate more surplus value than competing capitalists. The effect of constantly rising productivity of labor under capitalism is the replacement of living labor by machines. Under capitalism this happens in a manner that intensifies the exploitation of the workers rather than abolishing it. As Marx explains in volume three of Das Kapital:

“This mode of production produces a progressive relative decrease of the variable capital as compared to the constant capital, and consequently a continuously rising organic composition of the total capital. The immediate result of this is that the rate of surplus value, at the same, or even a rising, degree of labor exploitation, is represented by a continually falling general rate of profit. Later we will see why this fall does not manifest itself in an absolute form, but rather as a tendency toward a progressive fall. Therefore the progressive tendency of the general rate of profit to fall is just an expression peculiar to the capitalist mode of production of the progressive development of the social productivity of labor. This is not to say that the rate of profit can’t fall temporarily for other reasons. But proceeding from the nature of the capitalist mode of production it is thereby proved a logical necessity established that in its development the general, average rate of surplus value must express itself in a falling general rate of profit. Since the mass of employed living labor is continually on the decline as compared to the mass of materialized labor set in motion by it, i.e. to the productively consumed means of production, it follows that the portion of living labor, unpaid and congealed in surplus-value, must also be continually on the decrease compared to the amount of value represented by the invested total capital. Since the ratio of the mass of surplus value to the value of the invested total capital forms the rate of profit, this rate must constantly fall.”

Thus, as the proportion of capital invested in variable capital (living labor) falls in proportion to that invested in constant capital (dead labor), the proportion of total investment that generates a profit must decline. The build up of constant capital— fixed capital in machines, buildings, computer technology, software etc., as well as the circulating elements such as raw materials and semi-finished components— rises in proportion to living labor. The result is a tendency for the rate of profit to fall. The rate of profit is not the mass of profit generated in capitalist production, but the mass of profit relative to the level of investment. It is not the case that the mass of profit necessarily falls as the rate of profit falls. On the contrary, increased productivity boosts the mass of profit by expanding the scale of production. However, as productivity increases, capital becomes more centralized and concentrated, and dead labor increases relative to living labor. The worker now has more machinery at his or her elbow as the ratio of constant to variable capital constantly increases. So, as productivity rises, the organic composition of capital rises and the rate of profit falls.

The Boom- Bust Cycle

Capitalism is subject to periodic cycles of expansion and contraction. These are periods in which production and economic activity rise and fall. In the rising phase of the cycle profits increase, capital increases, and the rate of profit rises. But over the course of the cycle, capital starts to overaccumulate and the tendency for the rate of profit to fall kicks in. At a certain point in the boom phase of the business cycle, the next round of investment cannot generate a sufficient rate of profit to make it worthwhile to invest in new means of production. As the profit rate falls, investors withdraw their capital from a particular branch of production causing plant closures and lay offs. Or, they withdraw money capital from the financial system, causing a credit crunch. Or, they demand much higher interest for loans, causing bankruptcies and more credit problems. Or, they boost prices for fuel, food and other consumption goods. Wages are cut, unemployment increases, jobless workers put pressure on existing wage levels and workers’ standard of living falls everywhere.

This pressure on profit rates results from the overaccumulation of capital discussed previously. Because profit rates come under the most pressure in sectors with the highest organic composition of capital (those with the highest productivity, in which constant capital is highest in proportion to variable capital), the average rate of profit falls and new capital investment is deferred. The profitability crisis engenders a search for more profitable outlets for capital investment. Overaccumulation of capital at home drives the export of capital to less developed, lower wage countries where higher profit rates can be found because of lower levels of technology in use. It also drives capital into the financial markets to speculate in share values, or complex financial instruments like derivatives, credit default swaps, or into securitized investment vehicles like subprime mortgage bundles, or into commercial property speculation, and into the ever more reckless use of credit to keep the system afloat. Ultimately, it leads to the emergence of widespread forms of fictitious capital that are not related to the underlying value of real commodities.

There are factors that can offset the tendency for profit rates to decline. Marx called them “countervailing tendencies” acting to delay the tendency of the rate of profit to fall. In the absence of these counter tendencies capitalism would be in a permanent slump of ever falling profitability. David Harvey denies that the falling rate of profit causes crisis, arguing that the countervailing tendencies offset the general tendency. For Harvey, the tendency for profit rates to fall doesn’t cause crisis. On the other hand, the tendency suggests ways for capitalists to extract even more profit. In Capital v.3, Marx directly contradicts Harvey’s claim. And a growing body of empirical evidence presented by Marxists like Michael Roberts demonstrates that these tendencies cannot offset falling profit rates indefinitely. In the long run, the law asserts itself against the resistance of the counter factors. The tendency itself is the driving force while the counter tendencies are secondary attempts to restrain the law. Through the operation of these counter-tendencies, breakdown turns into temporary crisis, so that the accumulation process is not something continuous but takes the form of periodic cycles.

As noted above, due to the over-accumulation of capital and falling profitability, the boom phase of the business cycle turns into a bust phase. Falling investment results in recession:

● overproduction appears as monetary demand for commodities shrinks

● goods go unsold as inventories pile up

● production contracts causing a sharp rise in unemployment

● the weakest firms go under.

Money capital advanced on the assumption of yielding high returns is exposed as worth much less than anticipated. A credit crunch follows as bank loans and financial assets are revealed to be massively overvalued. The process of capital circulation comes to an abrupt halt, and the system seizes up as if gripped by a sudden heart attack. A traumatic process of devaluation of capital ensues. Different fractions of the capitalist class fight amongst themselves as to who will bear the costs. This does not take place in the abstract, or just on paper but across the world, affecting the lives and living conditions of millions.

A capitalist crisis is a violent and destructive process. Currencies are devalued, debts are called in, weaker countries have their credit lines frozen (i.e., Greece). Both the rate and the mass of profit fall and employers frantically seek out “excess” capacity to dump. Eventually, as less competitive capital is devalued, and constant capital is bought up on the cheap by the dominant firms, the rate of profit recovers, capitalists begin to reinvest in cheaper plant, machinery and workers. A recovery begins and the cycle begins anew.

How robust the upturn will be, or how quickly crisis and recession recur, depends on how successful the dominant monopoly capitalists are in making both the weaker capitalist countries and the working class pay the price of the crisis. And there can be strong resistance to this. But the answer ultimately depends on how much capital is devalued over the course of the crisis.

No Recovery after Twelve Years?

Why has there has been no sustained recovery from the financial collapse of 2008? In the space available, only the most cursory answer can be given. The falling rate of profit and the increasing concentration and centralization of capital can help illuminate the failure to recover, as well as the cause of the crisis itself.

The world economy remains in the doldrums as levels of investment remain about 25% below pre-crisis predictions for the most advanced economies. Following the Second World War the average rate of profit was 15%; in 1980, it was 10%; and, today it is stuck at 5%. Even former Treasury Secretary, Larry Summers, refers to the period following the crash of 2008 as “secular stagnation.”

Instead of clearing out dead capital, the system was put on life support. The government spent trillions of dollars bailing out banks and financial firms and purchasing toxic assets like corporate junk bonds and securitized sub-prime mortgages. Additional trillions of dollars were pumped into the central banks through quantitative easing policies, injecting a stream of ultra-cheap credit into the system. After all that we are now in another major depressive crisis, triggered by the COVID19 pandemic. This led to another multi-trillion dollar bailout of finance capital, and a half-trillion dollar handout to major corporations in the recent CARES Act. Official monetary policy is now “QE forever”!

A far greater devaluation of capital is required to pave the way to a new boom. The scale of capitalist firms, their interpenetration with the state and the financial system, and the transnational nature of capitalist finance, combine to render such a painful process more difficult than in past slumps. For example, 20% of non-financial US corporations are “zombie firms”, kept alive by continual infusions of new credit from banks at near zero interest rates. It must be stressed that we are not witnessing a final breakdown of capitalist production. It is still possible for areas of the world economy to expand, but it’s difficult to foresee a return of the high profit rate expansion of the ‘90s, to say nothing of a return to the sustained boom and 15% profit rates of the post-war “Golden Age.” In the years ahead we are likely to see either prolonged stagnation, or an even deeper economic crisis.

Another very real prospect is war. While the ruling class lacks the understanding of its own system to pursue war as a devaluation mechanism to destroy unprofitable capital, the imperialist world becomes more unstable and volatile. As the global crisis ratchets up tensions between rival powers, the nationally domiciled ruling classes vie to shift the burden of the crisis onto one another to garnish whatever share of the available surplus value they can. New economic powers like China have entered the world market demanding their own share.

The relative decline of US economic hegemony from 30% of global GDP in the post-war years to less than 20% today increases the danger of war. However, with over 35% of global arms spending, the US remains the most dangerous and predatory imperialist force in the world.

“Adam Tooze in his book “Crashed: How a Decade of Financial Crisis Changed the World” writes, the “financial and economic crisis of 2007-2012 morphed between 2013 and 2017 into a comprehensive political and geopolitical crisis of the post–cold war order”—one that helped put Donald Trump in the White House and brought right-wing nationalist parties to positions of power in many parts of Europe. “Things could be worse, of course,” Tooze notes. “A ten-year anniversary of 1929 would have been published in 1939. We are not there, at least not yet. But this is undoubtedly a moment more uncomfortable and disconcerting than could have been imagined before the crisis began.”

Conclusion

If we could imagine away the capitalist social relations of production, we could visualize what the dominant ideology obscures: improved technology and rising labor productivity should lead to a reduction of necessary working time. Mechanized production would free workers from the division of labor enforced by the law of value to become the planners of production, distribution and consumption. We would work as few or many hours as desired. But for this to happen the world working class would need to transfer ownership of the means of labor from the private property of a privileged few, to the social property of the vast majority of humanity. At the present moment of existential danger to which capitalism has brought humanity, it is fitting to end an article on his theory of crisis, by recalling Marx’s words on the historical tendency of capitalist accumulation in the 1st volume of Kapital:

“One capitalist always kills many. Hand in hand with this centralization, or this expropriation of many capitalists by few, develop, on an ever-extending scale, the co-operative form of the labor-process, the conscious technical application of science, the methodical cultivation of the soil, the transformation of the instruments of labor into instruments of labor only usable in common, the economizing of all means of production by their use as means of production of combined, socialized labor, the entanglement of all peoples in the net of the world-market, and with this, the international character of the capitalistic regime. Along with the constantly diminishing number of the magnates of capital, who usurp and monopolize all advantages of this process of transformation, grows the mass of misery, oppression, slavery, degradation, exploitation; but with this too grows the revolt of the working-class, a class always increasing in numbers, and disciplined, united, organized by the very mechanism of the process of capitalist production itself. The monopoly of capital becomes a fetter upon the mode of production, which has sprung up and flourished along with, and under it. Centralization of the means of production and socialization of labor at last reach a point where they become incompatible with their capitalist integument. This integument is burst asunder. The knell of capitalist private property sounds. The expropriators are expropriated.”

Glossary

Constant capital (c) = Means of production (fixed capital) and raw materials (circulating capital)

Variable capital (v)= Cost to the capitalist to purchase labor power to produce the commodities paid in wages

Surplus value (s) = The value labor expends to produce commodities over and above its own value in wages paid

Rate of Surplus Value (s/v)= The ratio of the surplus labor time, which the producing class works without pay, to the necessary labor time they need to maintain their standard of living. Also called the rate of exploitation

Organic Composition of Capital (c/v)= The “organic composition of capital” is ratio of the value of the materials and fixed costs (constant capital) embodied in production of a commodity to the value of the labor-power (variable capital) used in making it. Also called the ratio of dead to living labor

The Rate of Profit (s/c+v)= Profit as a percent of the total capital invested in production. ROP = S/C+V

It is only through and open and robust discussion scientific socialism, ie Marxism has developed. Classconscious.org would like to play its role in developing such a culture again. We are attempting to foster debate by publishing articles that may not fully align with the position of our editorial collective.